A few days back, Hon. Minister of Telecommunication & Digital Infrastructure Harin Fernando made an announcement on Facebook. He announced the conclusion of fruitful discussions to facilitate the entry of Stripe to the Sri Lankan market. Replying to one of the comments to his announcement, the Hon. Minister also mentioned that the proposal for Stripe to enter the Sri Lankan market has been finalized. Should the Central Bank approve the proposal, then ICTA would sort out the paperwork and Stripe would be operational in Sri Lanka within 2 – 3 weeks.

In case you’re lost, Stripe is a startup based in San Francisco that offers an online payment gateway for individuals and businesses. Founded in 2011, Stripe is valued at $5 billion and processes over $10 billion in transactions. Should the Central Bank approve the proposal, then Stripe’s entry to Sri Lanka would be a game changer for the local e-commerce industry. Why? Because the payment gateways we have in Sri Lanka are horrible.

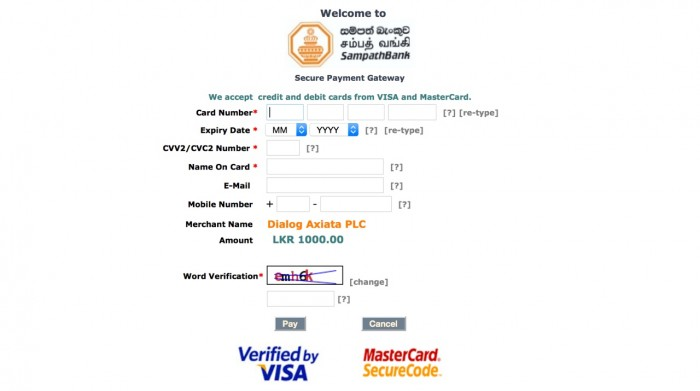

Currently, the only payment gateways in Sri Lanka are the ones offered by the banks. We did a preliminary scan of each bank’s offerings last year. There was no clear-cut offering, as with all things in life, the picture was a very gray one. However, no matter which option you pick, you still have to submit a proposal and if it’s approved you pay a hefty initial setup cost, yearly maintenance costs, commissions on each transaction and have to make a fixed deposit. Needless to say, our local payment gateways aren’t cheap and they’re horribly designed.

If you’ve ever used any local payment gateway, you’d have found that they look ugly and using them is a challenge. For local e-commerce companies, this is a huge problem. This is because if any part of the website it poorly designed, it can drastically reduce the number of sales a website makes. This problem becomes worse when you realize that the local e-commerce companies lose sales, without having any say about the design of these payment gateways. In other words, local e-commerce companies pay a ton of money, only to get a payment gateway that looks like it hasn’t been updated since the 90s.

Another issue with online payments in Sri Lanka is accepting international payments. Today, it’s all too common across the world to use trusted services such as PayPal for online transactions. However, as we all know, you still can’t receive money using PayPal in Sri Lanka. As we just discussed, our local payment gateways with their horrible design kill many potential sales. When analyzing the international context, this isn’t an issue faced only by local e-commerce companies but also skilled freelance workers. This is why many of them have been asking the government to bring PayPal to Sri Lanka for years.

However, it was only until last month that we saw some progress. We saw the regional head of PayPal visit Sri Lanka to discuss inward payments and the central bank removing all obstacles that previously prevented services like PayPal from operating in Sri Lanka. And then we heard nothing.

Once again, we were left with hoping PayPal would come to Sri Lanka. We saw talks happening but zero action. With the announcement of Stripe, we finally got an answer as to why this was the case. According to Hon. Minister Harin Fernando’s comments, PayPal had said that they weren’t interested in entering the Sri Lankan market because it was too small. The Hon. Minister further commented that dialogue is still open between Sri Lanka and PayPal with negotiations taking place to launch it in Sri Lanka next year.

While talks are happening, it could take at least a year until PayPal launches in Sri Lanka. But now we have a powerful alternative to PayPal potentially coming to Sri Lanka. So how does Stripe stack up to PayPal? Well, let’s take a look.

Stripe vs PayPal

When it comes to accepting online payments, Stripe has one basic offering that’s localized for each country it operates in. In the US PayPal has two offerings: PayPal Payments Standard & PayPal Payments Pro. However, when you look at what PayPal offers India, then the picture changes with two completely different offerings available: Website Payments Standard and PayPal Express Checkout.

Unlike the US offerings the only difference between the Indian offerings is that PayPal Express Checkout allows you to create custom payment pages. Beyond this, there are no differences between Website Payments Standard and PayPal Express Checkout. For the purpose of this analysis, we’ll be comparing Stripe’s Singaporean version and PayPal’s Indian offerings.

Trustworthiness

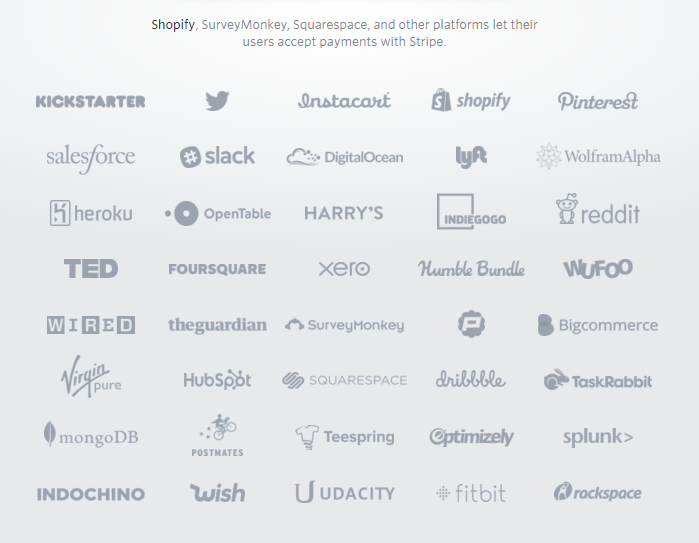

When it comes to online payments, PayPal is a well-recognized and trusted name. Stripe on the other hand, isn’t as well-recognized. We’re pretty sure that some of you only got to know about Stripe today. Yet Stripe deals with over USD $10bn worth of transactions. So what are the companies that trust Stripe to handle their money? According to the Stripe website, here’s a list of these companies that trust Stripe.

Stripe does have a large list of prominent companies that trust it. However, it’s going to take more than these names to overcome the image of trust PayPal has built over the years.

The commissions

The good news is that unlike our local payment gateways, both Stripe and PayPal don’t have setup or monthly fees that need to be paid. The only cost you’d need to pay if you use either service is the commission on each transaction.

If you use Stripe then you’d need to pay 3.4% + 50 cents (SGD) for each successful credit/debit card transaction. There are no additional fees for international cards, failed cards or any refunds you have to make. Additionally, if your business makes over (SGD) $100,000 a month then a lower commission can be negotiated. All you have to do is drop an email to the Stripes sales team.

However, if a dispute arises then you incur a (SGD) $15 fee unless it’s resolved in your favor. Stripe also supports bitcoins and charges 0.8% per transaction but it has a $5 price cap on all Bitcoin transactions. Furthermore, a failed bitcoin transaction will cost you $4.

PayPal on the other hand charges 4.4% + 30 cents (USD) for each sale. However, if you sell on eBay then you are charged 3.9% + 30 cents (USD) per transaction. You can get a discounted commission rate if your business qualifies for PayPal Merchant rates. Yet, even with merchant rates the lowest commission you can get is 2.9% + 30 cents (USD) for each sale.

Initially, Stripe seems to be the cheaper option for anyone accepting online payments. However, as the business scales, PayPal would become the cheaper option to implement.

The design

One of the biggest problems with local payment gateways is their horrible design. If you’re running an e-commerce website, then it’s vital that you are able to design a checkout page of their choice. So how do Stripe and PayPal fare in this regard?

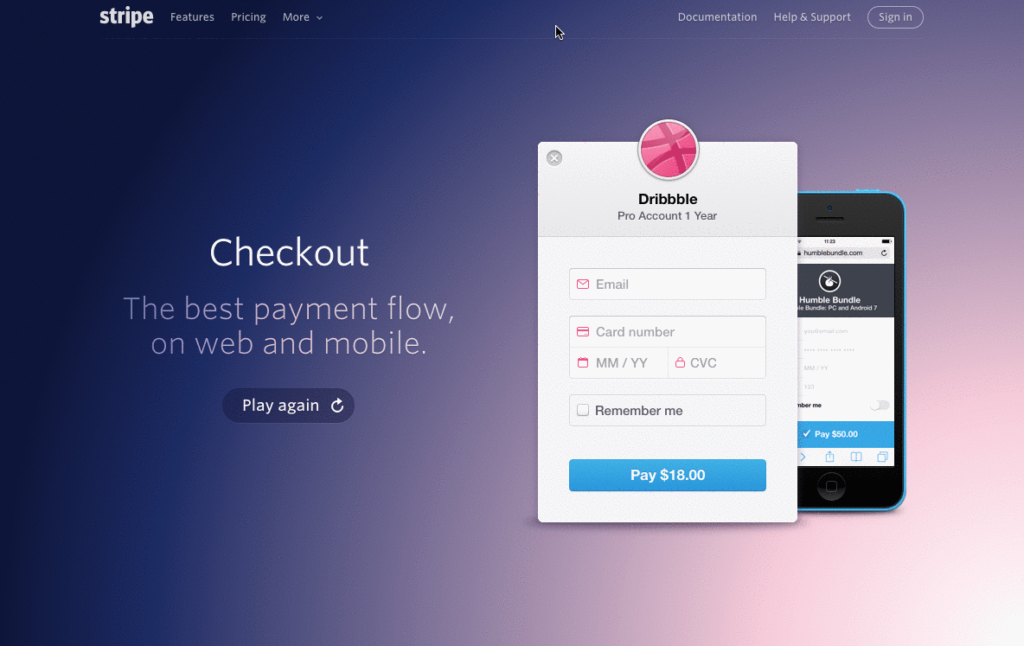

Stripe offers two options for checkout pages on your website. The first option is Checkout, which is a customizable form designed by Stripe that you can add to your website to accept payments. The second option is using the Stripe.js JavaScript library on your website. This library allows you to create a customized checkout page while it takes care of securely transmitting credit/debit card details.

Similarly, PayPal Express Checkout allows you to create a customized checkout page. With PayPal Express Checkout, for a brief moment, your users will be redirected off your website for them to log in to their PayPal accounts. This login process is similar to Facebook sharing.

When it comes to checkout pages, the winner is debatable. Unlike PayPal Express Checkout, with Stripe.js users aren’t redirected to another page to enter their details. Instead, on one page they can enter their details and checkout. However, one can’t deny that despite the extra redirect PayPal adds, with it’s trustworthy image, it can help increase conversion rates. The clear answer to this question will probably require a bit of trial and error. Nonetheless, both options would allow you to create a custom checkout page that will look significantly better when compared with existing local payment gateways.

Security

When it comes to online payments, security is paramount. Both PayPal and Stripe are PCI certified which means that they are both stable and secure platforms. However, as Memberful points out, Stripe actively encourages good security.

By using the Stripe.js library, an e-commerce company never has to store credit/debit card information of its customers. Instead, the data is directly sent to Stripe for processing. In contrast, PayPal requires the data to go through the e-commerce company’s servers before it’s sent to PayPal processing. This extra layer of security provided by Stripe may never stop a determined hacker, but it does make the process of stealing credit/debit card details harder.

Implementation

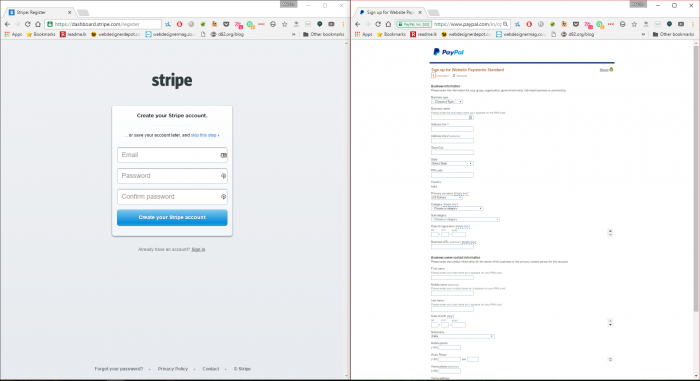

Finally, let’s say after your research, you’ve chosen which payment gateway you want. Assuming both PayPal and Stripe start working in Sri Lanka, you now have to implement the payment gateway on your website. Naturally, you want this process to be quick and clean. Now you might think both Stripe and PayPal would have similar procedures to sign up and use their services. The truth couldn’t be further from it.

Needless to say, Stripe easily wins when it comes to registration. Yet, it should be noted that registration is only the first step to implementation. There are other more technical steps involving a bit of coding. Thankfully, unlike our local payment gateways, both Stripe and PayPal have APIs with in-depth documentation on using them.

Final thoughts

PayPal is still the trusted and preferred mode of accepting online payments. However, upon analysis, Stripe does look like a viable if not a better alternative. It costs less, offers custom checkout pages, better security and is easier to sign up for. Should Stripe enter the Sri Lankan market, it would definitely be a massive game changer for local e-commerce companies. However, that is assuming the Central Bank approves the proposal.

Nonetheless, one has to commend the efforts of Hon. Minister Harin Fernando and ICTA CEO Muhunthan Canagey. When PayPal said no, they sought out an alternative to help our local e-commerce industry and skilled freelancers accepting international contracts. Hopefully, this saga will end on a happy note with the Central Bank approving the proposal and Stripe entering the Sri Lankan market.

Why we need a foreign startup to accept online payments? Can’t any of Sri Lankan Startups do this? Using Stripe or PayPal will shoot a lot of money to overseas for their transaction charges which further downgrades the rupee. If we can accept those payments locally that really helps the rupee. Isn’t it?

If a Sri Lankan startup had tried this Central Bank wouldn’t have authorized it nor ICTA helped this much. Attitude of a former colony i guess.

Sampath Bank offers a number of payment options including direct account payment etc.

And just so you’d know the new IPG at Sampath Bank is customisable to match the site.

Even though local banks charge annual fees, the transaction cost is low. Comparatively both stripe and PayPal charge exorbitant amounts for transactions and typically take 2 – 3 weeks to send the money.

Also disputes and chargebacks are normally biased towards first world countries.

It’s been almost 2 months and stripe is still not happening. Initially we thought it’s come in couple of weeks. WHy things are like this way in SRi Lanka 🙁

Just the talks and a selfie! Don’t forget this was initiated by a bunch of politicians and political appointments.

Anyupdates on strip or PayPal sri lanka?

Sri lanka will never have strip or PayPal. for PayPal the volume is too low. on the surface looks like many would use but in relality only a few would be sellign high volume to make sense for any payment gateways.

WOW. It’s been nine months and still I can’t see our country! what a joke!

It’s 2019 now and still no luck… 🙁

We’re almost at the end of 2017 and still, Stripe is not available for businesses in SL!

Sadly

another volkswagen factory :3

Even our banks don’t have their own payment gateway. They are using Australian payment gateway to process transactions.

We are now in the 2nd half of 2018 and we still don’t have either of these services. It is silly to even talk about creating our own alternatives when no customer would use their credit card on an unfamiliar payment gateway.

It’s a very long 2 weeks, I guess

So it seems